Reuben B.

Robertson Collection

M1977.13.03.4a

03

4a

01

[robt_002a]

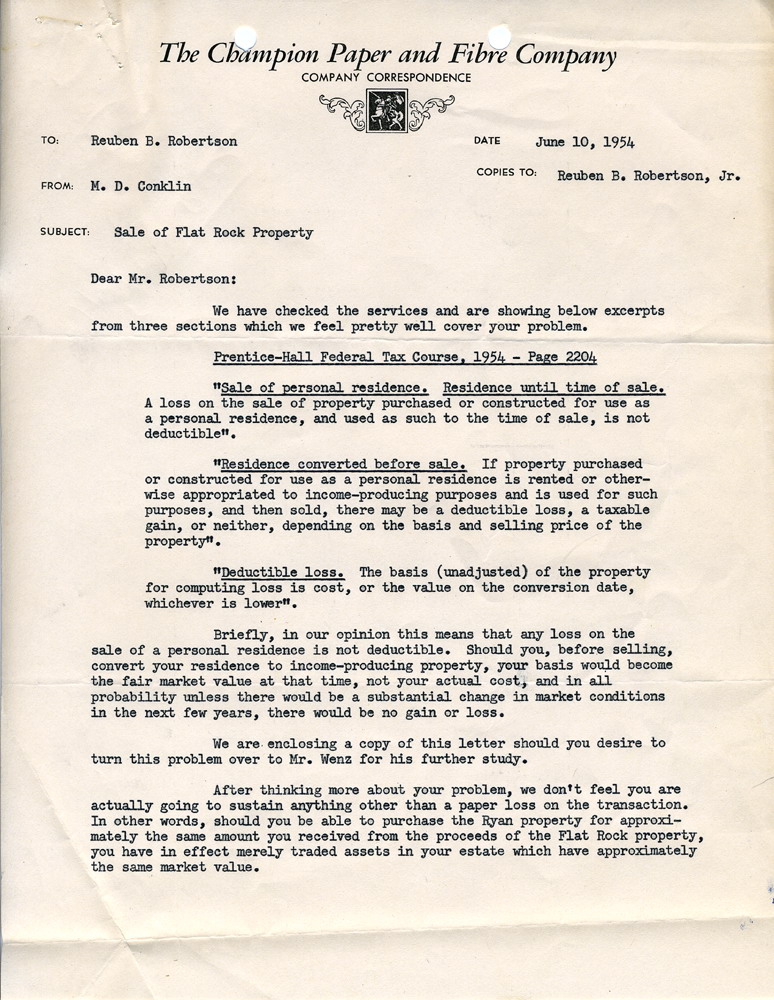

The Champion Paper and Fibre Company

Company Correspondence

June 10, 1954

To: Reuben B. Robertson

From: M. D. Conklin

Subject: Sale of Flat Rock Property

We have checked the services and are showing below excerpts from three sections which we feel pretty well cover your problem.

Prentice-Hall Federal Tax Course, 1954 - Page 2204

"Sale of personal residence. Residence until time of sale. A loss on the sale of property purchased or constructed for use as a personal residence, and used as such to the time of sale, is not deductible."

"Residence converted before sale. If property purchased or constructed for use as a personal residence is rented or otherwise appropriated to income-producing purposes and is used for such purposes, and then sold, there may be a deductible loss, a taxable gain, or neither, depending on the basis and selling price of the property."

"Deductible loss. The basis (unadjusted) of the property for computing loss is cost, or the value on the conversion date, whichever is lower."

Briefly, in our opinion this means that any loss on the sale of a personal residence is not deductible. Should you, before selling, convert your residence to income-producing property, your basis would become the fair market value at that time, not your actual cost, and in all probability unless there would be a substantial change in market conditions in the next few years, there would be no gain or loss.

We are enclosing a copy of this letter should you desire to turn this problem over to Mr. Wenz for his further study.

After thinking more about your problem, we don't feel you are actually going to sustain anything other than a paper loss on the transaction. In other words, should you be able to purchase the Ryan property for approximately the same amount you received from the proceeds of the Flat Rock property, you have in effect merely traded assets in your estate which have approximately the same market value.

Cordially yours,

Conk